Act now or pay later: Why boards must own climate risk and drive climate action

Impact Futures’ Brian Gidudu on why climate risk belongs in the boardroom, not the sustainability report.

For too long, climate risk has sat on the fringes of corporate decision-making – treated as a sustainability concern, reporting obligation or something that could simply be dealt with later.

That thinking belongs in the past. Why? Because climate risk is a financial and operational issue that affects cash flow, asset values, insurance costs, supply chains, financing, and the long-term viability of projects and business models.

How boards respond will determine which companies build resilience and which are left exposed to an obsolescent business model, product or asset.

That shift matters because it changes who bears the consequences. It is board members, not sustainability teams, who make the calls that determine whether a company can get insurance, secure financing, and keep its assets viable as climate conditions worsen. Get those calls wrong, and the costs are real: stranded capital, rising debt, obsolescent assets that lenders, tenants and customers will not touch.

The numbers don’t lie.

The gap between boards that understand this and those that do not is already measured in valuations, credit ratings, and regulatory fines.

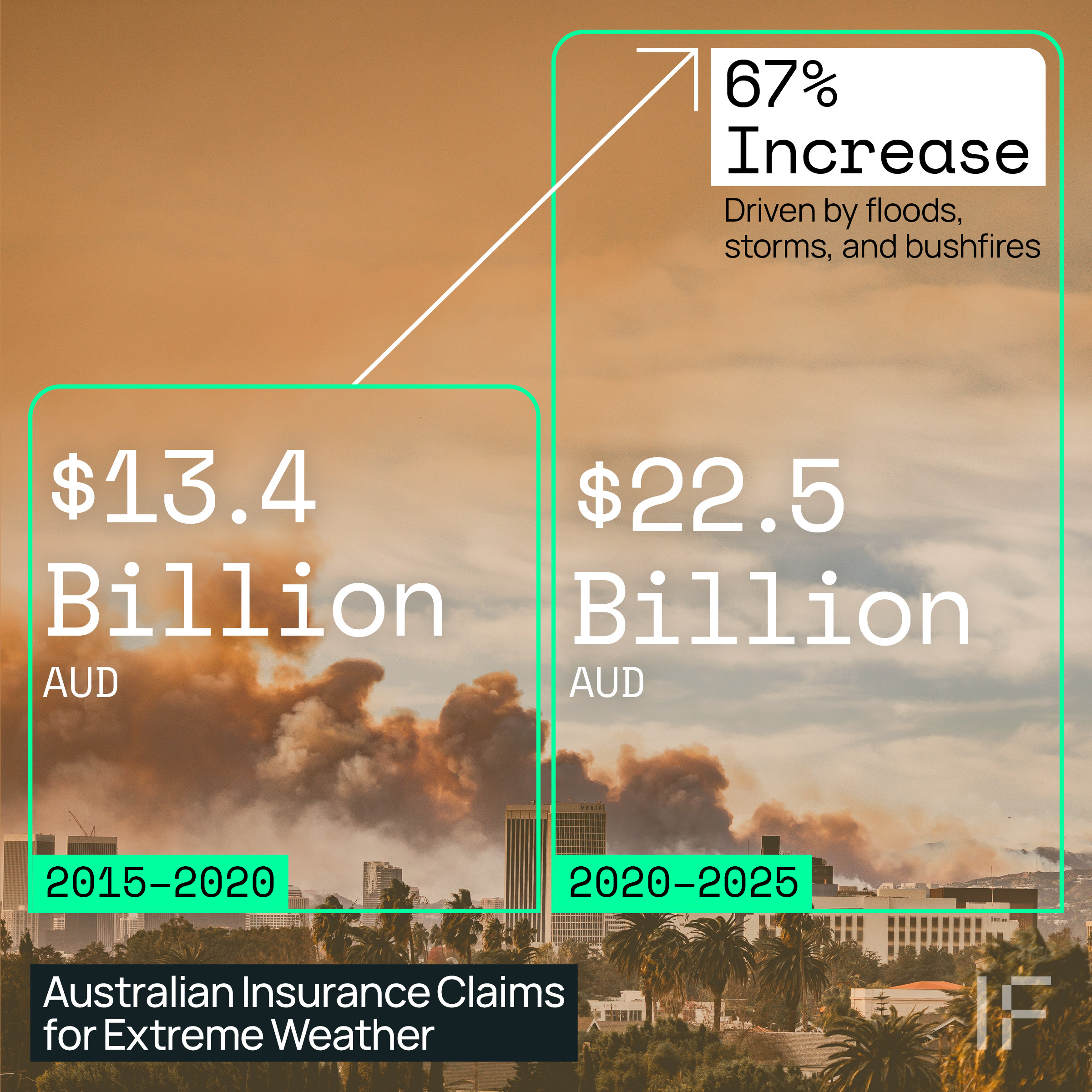

Insurance markets were the first to feel it. Premiums are climbing, coverage is shrinking, and in some locations insurers are simply walking away. The numbers from 2025 tell the story plainly: secondary perils — hail, floods, fires — accounted for a record 92% of all global insured losses . These are not rare catastrophic events. They are the everyday weather that is quietly making parts of the world uninsurable . Australian insurers paying over $22.5 billion in claims for extreme weather between 2020 and mid-2025. This marks a 67% increase compared to the previous five years, driven by floods, storms, and bushfires.

Regulators are moving with equal force. In February 2026, the ECB fined French lender Crédit Agricole €7.55 million ($12.5 million AUD) for failing to adequately assess climate risk within its lending portfolio, giving them just 75 days to fix it . That fine did not land on a sustainability team. It landed on the institution. Major financiers are taking note too – Bank of America’s 2025 climate disclosures now stress-test how extreme weather and policy shifts could affect the businesses it lends to.

These examples, and many others like them across the globe, make one thing clear: climate risk is already a financial event. The only variable left is whether boards are ready for it.

Two expensive risks.

The easiest way to understand climate risk is to separate it into two categories: physical risk and transition risk.

Physical risk covers the direct effects of extreme weather — floods, bushfires, heat, drought and rising sea levels. Transition risk comes from the shift to a lower-emissions economy: carbon pricing, tighter regulation, changing customer expectations, and pressure from lenders and investors. In both cases, climate risk becomes financial risk when it changes projected earnings, raises operating costs, shortens asset life, or forces unplanned capital spending.

Here is how both risks play out in practice. When extreme weather hits, businesses in vulnerable sectors can be forced to sell assets quickly and lose access to borrowing almost overnight . A commercial building in a flood-prone area that becomes uninsurable is a good example – without cover, banks will not lend against it, refinancing becomes difficult, tenants are harder to secure, and the value of the asset falls.

Transition risk works differently but hits just as hard. The EU now charges importers a fee based on the carbon produced in making products like steel and fertilisers, and in Q1 2026 that fee sat at €75.36 per tonne. For Australian steel or fertiliser producers exporting to the EU market, that kind of additional cost can materially alter financial performance.

The resilience advantage.

The boards making the most progress are not just managing climate risk, they are using it to build resilience that competitors will struggle to match.

Maersk, one of the world’s largest shipping and logistics companies, offers a clear example. Its $2 billion investment in a green methanol fleet was not a sustainability initiative but rather a calculated decision to get ahead of tightening carbon regulation, insulate operations from future regulatory costs, and secure long-term contracts with customers who now require Scope 3 compliance . The move protects a significant share of revenue from being locked out of decarbonising markets, and leaves Maersk better positioned than competitors still waiting to act.

The same logic applies to physical risk. If you are developing a 30-year asset in a flood or fire-prone area, the question is simple: will it remain insurable over its lifetime? If the answer is no, the financial consequences follow fast. An uninsured asset is far less attractive to lenders, and valuations can drop 30-40% as a result.

Ready or Not: The case for acting now.

A board that treats climate as a reporting exercise may meet compliance requirements and still leave the company exposed. A board that treats climate as a strategic risk will ask harder questions:

-

- Which existing assets are most exposed to physical damage or uninsurability?

- Which planned projects depend on climate assumptions that no longer hold?

- What happens to bottom line if the CBAM price hits €120 per tonne?

- How does a 3°C or 4°C warming scenario affect insurance premiums, supply chain resilience, and financing terms for your largest projects?

If you are sitting on a board or in a leadership position, here is how you move past simple compliance:

-

- Embed climate in enterprise risk management: Integrate climate scenarios into capital planning and insurance strategy, not just annual reports.

- Climate-adjusted approvals: Test every major project for lifecycle resilience against physical and transition risks.

- Quantify the risk: Calculate the actual revenue loss from a 1-in-100-year flood at your largest facility.

- Follow the capital signal: Treat lender requests for climate and emissions data as credit risk signals, not a compliance checklist.

- Break the silo: Bring sustainability expertise into the room where capital and P&L decisions are made.

- Screen your supply chain: Use procurement as a first line of defence against climate exposure.

- Link incentives: Tie executive bonuses to climate-adjusted returns, rewarding resilience not just short-term financial targets.

The companies that do this well will not just be ahead on compliance. They will be more insurable, more financeable, and better placed to hold and grow value as conditions tighten. Reporting matters, but it should be evidence of good governance and the resilience that comes with it, not a substitute for it.

The call to action for boards is simple: own this. The financial system has already priced climate risk into insurance premiums, credit ratings and lending decisions. The only question left is whether your boardroom has caught up.

Thought Leader

Brian Gidudu

Senior Sustainability Consultant

Sydney

Brian is a sustainability specialist with over eight years of experience across five continents, helping organisations navigate the intersection of climate change, nature loss, and pollution. Brian finds genuine satisfaction in helping organisations translate complex regulatory requirements into actionable strategies that future-proof them against potential risks while meeting their growth and investment goals.

Having worked with organisations such as Pangolin Associates, the Carbon Trust, and the United Nations Environment Programme, Brian has a proven track record of delivering complex GHG measurements, decarbonisation pathways, climate risk assessments, and capital climate alignment across the manufacturing, education, infrastructure, banking, mining, transport, and energy sectors. His technical expertise spans global reporting frameworks and standards, including ASRS, NZ-CS, CSRD, IFRS, GHG Protocol, Climate Active, Toitu, NGERS, PCAF, SBTI, and NZIF. He possesses unique expertise in bridging the gap between high-level ESG strategy and ESD, ensuring that investments are resilient to both the physical and transitional risks posed by a changing climate and nature.

Media Contact

Suhanna Yazami Gildea

Global Insights & Communications Specialist

Suhanna is Impact Futures’ Global Insights and Communications Specialist. She works across the 7C Network to help leaders and specialists clearly communicate the value and impact of their work, ideas and thinking through insights that are focussed and relevant. Her work centres on translating complex ideas into engaging narratives that shape how the built environment responds to future challenges.